|

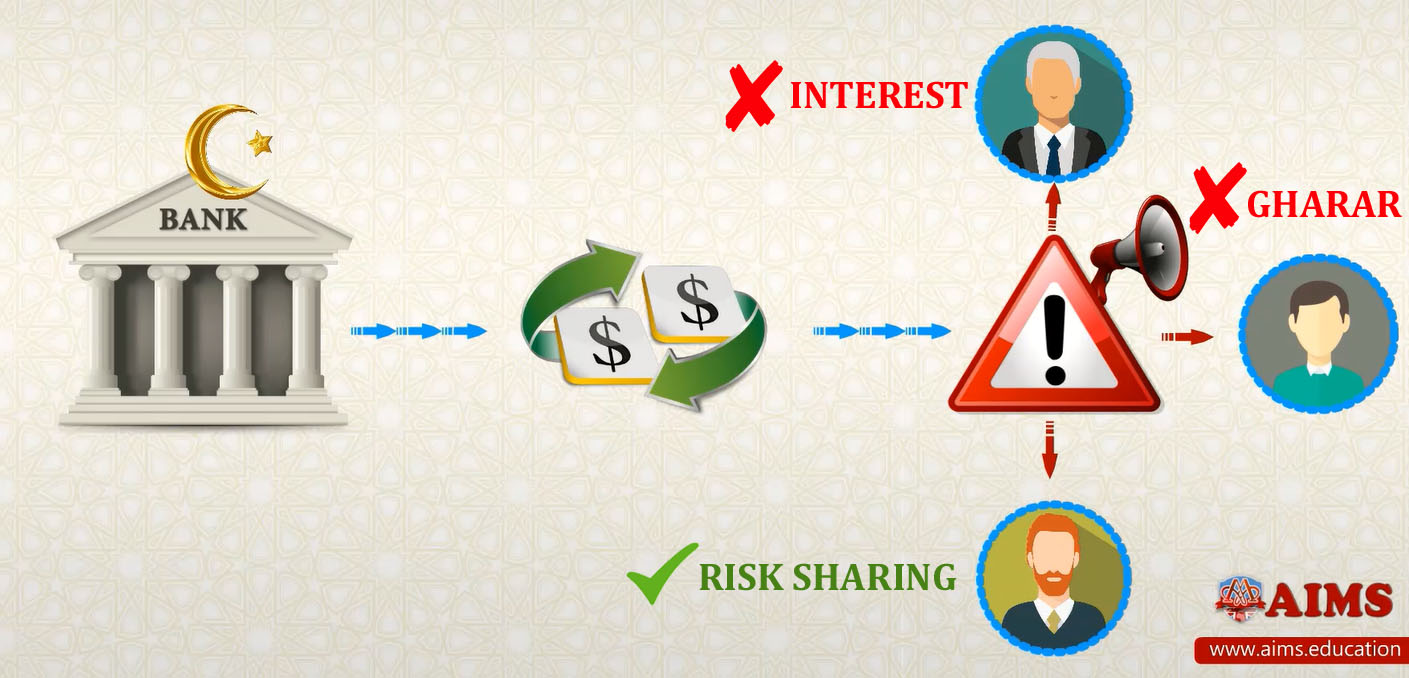

ANU utilises MyTimetable to enable students to view the timetable for their enrolled courses, browse, then self-allocate to small teaching activities / tutorials so they can better plan their time. If you have been offered a Commonwealth supported place, your fees are set by the Australian Government for each course. More information about your student contribution amount for each course at Fees. To date, Victoria is the only state to recognise the potential for Islamic finance contracts to incur double stamp duty, introducing legislative exemptions in 2004. “One of the great challenges in starting Australia’s first Islamic bank is that you have all of these jurisdictional and legislative Sharia Loans Australia challenges that you don’t have when you’re running a conventional bank,” Mr Gillespie said. Designed to meet Islamic Law requirements, the product structures financing as a lease where ‘rent’ and ‘service fee’ are paid instead of ‘interest’. The Bank has also invested in achieving the endorsement of Amanie Advisors, a global Shariah advisory firm on behalf of its customers to provide comfort around the law compliancy while saving clients valuable time and money. However, according to Ernst & Young, Islamic banking assets have experienced rapid growth and are forecast to increase by an average of 19.7% a year until 2018. A number of Australian financial institutions have examined Muslim financing concepts such as profit sharing and rent to buy while trying to avoid terms such as "interest" in contractual agreements. With around 1.7% of the Australian population being Muslim, there are limited Sharia-compliant home finance programmes on the market. As general manager of Iskan Finance, Russell Murphy states, “For our customers, at the date of settlement, they are registered as the owner. We’ve taken the mortgage from them, and secured a transaction agreement that doesn’t express principal or interest. "Islamic Finance providers can structure financing in such a way to overcome this barrier, opening up financial and housing choices that would otherwise isolate Muslims from the rest of the population." Only four R-ADIs have been granted, and one licence has already been handed back after the institution, Xinja, failed and had return all of its customers' money. A R-ADI is a transitional banking licence that APRA introduced a few years ago to allow smaller operators to enter the market. Now two small local entities are trying to have another crack at setting up an Islamic bank in Australia using a new form of banking licence set up by the financial regulator, APRA. "So a lot of these investors, as the industry has developed, will be looking to diversify their funds and look for alternative investment location. Australia is well placed in all of that." To get started we will conduct an initial pre-assessment to determine how much we can finance you and whether you will fit the requirements for eligibility. The information you provide us here will be verified with supporting documents which we will ask you to provide later. We are rigorous about ensuring the Shariah integrity of our products through Shariah audits and on-going testing. MCCA has long supported the Bachar Houli Foundation, with the new community partnership set to extend the relationship and support the development of more role models in the Islamic community. If you have concerns or in need of financial help,get in touch with our team today. If you have any concerns or in need of financial help, get in touch with our team today. The way it works is that the financial institution mortgages the property and charges you an amount that you pay in rent. The more funds you repay, the more ownership you have in the property until it is paid off in full. Keep in mind that just because the institution doesn’t charge interest, doesn’t mean it doesn't charge a profit. The financial institution still makes a profit from leasing the property to you. The providers of this style of finance all operate under the National Consumer Credit Protection Act and will make independent enquiries into your ability to meet the financial commitments without undue hardship. This often means Islamic finance comes in the form of a “ full doc” application process.

In fact, the World Economic Forum recently ranked Australia as the second among the world's financial centres, behind only the United Kingdom, primarily due to the stability of our financial institutions over the past 12 months. The tax treatment of Islamic financial products should be based on their economic substance rather than their form. Fees and charges may apply, as well as terms and conditions which you should review. In order to open a credit product in future, you will need to meet our credit criteria and be approved. Please review the product disclosure documentation provided at the time of opening your account for detailed information. The term ‘Islamic Banking’ is a constituent of ‘Islamic Finance’ and refers to the set of banking and financial rules and practices organized on a basis that excludes interest as a determinant in financial lending and borrowing transactions. The conceptual basis of interest-free banking is to be found in Islamic tenets or Shari’ah. The latter encourages the practice of ‘Profit/Loss Sharing’ as opposed to interest . "The question for them arose whether they could actually undertake the Islamic banking activities within the Australian framework. And the decision was made that that was quite a difficult prospect." Some time ago, Amanah Finance's Asad Ansari consulted for an offshore Islamic bank that was interested in setting up a branch in Australia. Imran says NAB isn't looking to play in the consumer Islamic finance space. He believes the big opportunity for Australia is setting up mechanisms that can allow offshore companies to invest here. "I'm a Halal butcher, with a Halal investment, and a Halal superannuation." PRESS RELEASE: Australia's first-ever Islamic bank is here Media Database Islamic Bank Australia just happens to be the first one in Australia. Dr Imran Lum, Director Islamic Finance in NAB’s Deal Structuring and Execution team said; “We’re really proud to be able to offer such a valuable service to Australia’s Muslim community. "People could pay their bills with us, withdraw at ATMs, have savings with us on a profit-share basis, not interest based." Moreover, before you apply for a specific loan, please make sure that you’ve read the relevant T&Cs or PDS of the loan products. You can also check the eligibility requirements to determine whether the product is right for you or not. The financial institution makes money by charging a profit rate on your rental instalments. In most cases, you are offered the same features as a typical home loan. Some of these help you in achieving property ownership sooner, while others can give you the option of lower payments if you make lease payments only. This is because they believe that both Islamic and conventional banks make the same return, except conventional banks label it "interest" while Islamic institutions label it "profit". However, you must consider additional concepts such as risk-sharing and the absence of ambiguity which make Islamic home loans unique, compared to traditional loan products. On this subject, Murphy states, “In Australia, the Muslim community comprises Pakistanis, Fijians, Indians, Malaysians, Egyptians and so on. It would not be uncommon for some people to come to me and say ‘I want my Imam to sign off on your program’. This paper explores the nature and extent of financial exclusion of Muslim community in Australia. Adopting a survey questionnaire method primary data has been used, and Queensland is the selected state for this exploratory case study. While nearly 3 billion people in the world face difficulties in accessing formal financial services and products, in Australian alone, approximately 3.1 million of the adult population are identified as being financially excluded. “Our proposition is a segment-based proposition for Muslim Australians. We’re not just designing a digital experience; they’re fundamentally different products,” Mr Gillespie said. Then instead of having mortgage repayments, you’ll be paying rent as if leased. The cost will include the rental amount plus payment towards buying the bank’s ownership of the property. MCCA Islamic Home Finance Australia Shariah Compliant Halal Finance Muslim mortgage Our products have been developed in close collaboration with some of the world’s leading Islamic finance scholars. These have included, Datuk Dr Daud Bakar and Professor Sheikh Ali El Gari . That said, after several years of working with scholars, Australia lawyers, regulators and suitable funding sources, we opened our doors to the public with our Islamic finance solutions in 2015. Learn how we provide authentic Sharia compliance with our industry-leading Islamic finance offering. The LVR ratio refers to the amount of the property value or purchase price you can borrow from the lender. A loan with a high insured LVR allows you to borrow funds without paying lenders mortgage insurance . With its current APRA restricted licence, Islamic Bank Australia can only have a limited number of customers in 2023. National Australia Bank today announced that it has invoked its disaster relief package for customers impacted by bushfires in the Perth Hills area of Western Australia. This service may include material from Agence France-Presse , APTN, Reuters, AAP, CNN and the BBC World Service which is copyright and cannot be reproduced. "One of the great things about Australia is we live in a nation where so many different people from different cultures or different religious backgrounds, or even no religion at all, can get on." Homebuyers agree to enter an agreement with a finance company where each party will have part ownership of a property until the loan is repaid in full. Only four R-ADIs have been granted, and one licence has already been handed back after the institution, Xinja, failed and had return all of its customers' money. The product uses a similar arrangement to the Islamic home loans, with a combination of rental arrangements and fees. Its new Sharia-compliant financing product specifically targets transactions over $5 million for commercial property and construction. Our goal at Mozo is to help you make smart financial decisions and our award-winning comparison tools and services are provided free of charge. However, no matter how it is worded, not all Muslims see the Islamic finance banking institutions as true followers of Sharia. Instead, say critics, they are the same as the banks they claim to offer an alternative to, still taking in profit and cloaking "interest" under a different name and using external funders that don't practice Sharia. Islamic finance company to offer full suite of lending products National Australia Bank has launched a range of business finance products suitable for Islamic business borrowers. Islamic banking is unique as many aspects of the traditional Australian financial landscape are not halal, or permissible, under Islamic law. Borrowing on interest, for example, is generally considered as not being allowed in Islam. One of the largest mortgage aggregators in Australia, Finsure, has paired up with Hejaz Financial Services to offer mortgage broking service to the Australian Muslim homebuyer market for the first time. The Islamic Bank has an agreement with the traders for financing and one of the main functions of the bank is to monitor the profit and loss accounts of the traders concerned. That individual can buy an asset or manage the money through investments. The issuer of the Sukuk and the buyer can share ownership of the asset. The investor does not have a debt obligation to the issuer. For investment options that help grow your wealth while being Islamically sound, MCCA has the right options for you. To help you navigate the complex world of finance, insurance and utilities, we are committed to offering you a free service to help find you the right product to suit your needs. The prohibition on ambiguity often means that your provider Islamic Bank Mortgage will want to see very clear evidence that you can pay your mortgage and that you have a long history of sound financial management. Most Islamic mortgages have broadly the same features as regular products, including the option to overpay or even just to pay the lease amounts. How your loan to value ratio affects the amount you can borrow and how much your subsequent payments will be. As time goes on, the investor pays the bank some money and the bank transfers its equity to them. Fees and charges may apply, as well as terms and conditions which you should review. In order to open a credit product in future, you will need to meet our credit criteria and be approved. Dr Imran Lum, Director Islamic Finance in NAB’s Deal Structuring and Execution team said; “We’re really proud to be able to offer such a valuable service to Australia’s Muslim community. If you need to explore your options, you Islamic Bank Australia may want to speak to a mortgage broker. They have the necessary knowledge and experience to help you find the best lender that meets your needs, preference, and budget. The first dealer then owes the second dealer the amount of money they transferred. It is informal, meaning that arrangements are based on trust and not official contracts. There is a vigorous debate about whetherinsurance is halal or haram. Some Islamic scholars do argue that traditional insurance is permissible because the intentions of insurance are good. But a Muslim can err on the side of caution and focus on cooperative insurance. Commission share on referrals to third party advice providers (mortgage/finance/insurance broker, financial adviser, financial institution, utilities provider or any other third party). Income could be an Sharia Bank Loans upfront commission and/or ongoing commission. The commission depends on the amount of the finance, cost of the product or other factors and may vary from product to product. The new Islamic banking technology prototype will allow Australian financial institutions to plug in and provide personalised Islamic services to their customers, across savings and transactions accounts, and lending. The salient benefit of an Islamic finance facility is that there is an ethical overlay applied to it, whereby both loan funding and loan purpose have an ethical requirement. Moreover, the mortgage products can be highly competitive with rates offered by many conventional non-bank lenders, and in some cases, may be cheaper than those offered by non-Islamic lenders. Consider whether this advice is right for you, having regard to your own objectives, financial situation and needs. You may need financial advice from a suitably qualified adviser. For more information, read Canstar’s Financial Services and Credit Guide and our detailed disclosure. Find out the latest insights about super, finance and investments. We congratulate you for making the right choice and selecting the halal home loan alternative. Once you have completed and submitted this form, a dedicated MCCA sales executive will contact you within 1 business day to walk you through the next stage of your application. By providing you with the ability to apply for an insurance quote or a credit facility we are not guaranteeing that your application will be approved. Your application is subject to the Provider’s terms, conditions and criteria. It’s rare for institutions to suggest Islamic mortgages to non-Muslims simply because there’s not much extra benefit to be had if you’re not concerned about adhering to religious principles. We provide tools so you can sort and filter these lists to highlight features that matter to you. Belinda Punshon worked for Finder as a writer on home loans and property and as a corporate communications executive. She has a Masters in Advertising, Public Relations and Journalism from the University of New South Wales and a Bachelors in Business from the University of Technology Sydney. Look for a lender that offers weekly, fortnightly or monthly payments so you can arrange your payments to suit your income. “Islamic finance is largely about the philosophical side of things – it’s where Western banking meets Islamic banking. We offer an alternative solution for Muslims in an Australian landscape. Major aggregator teams with Islamic finance provider to create Aussie first Depending on the financial institution, Islamic home loans may be slightly more expensive than non-Islamic home loans. However, this will depend on how the financial institution determines the profit made on the sale. The fundamental difference between a typical home loan and a Sharia-compliant home loan is in the borrowing terms used (i.e. interest with a typical home loan vs rental or profit fee with an Islamic home loan). The bank has security over the property, which means that if the borrower defaults on their home loan, the lender can enforce a sale of the property to recover the outstanding funds that are owed. "People could pay their bills with us, withdraw at ATMs, have savings with us on a profit-share basis, not interest based." The bank has legal claims to the home, and can repossess and force you to sell it if you default on your loan.

However, he acknowledged that some people were skeptical or critical of whether Islamic banks were taking "interest-bearing" interest in the name of "halal business". Nestegg will keep you Islamic Bank Home Loan informed about the latest in banking, credit cards, and loans. With our wide-range of comprehensive content, you can get all the information you need on how to borrow money more effectively. According to research by Hejaz Financial Services, as much as 36 per cent of Australian Muslims opt to hold onto savings in cash due to the lack of Sharia-compliant products and services. Sukuk can only be used on ethical investments, not things that are considered haram – forbidden by Islam – for example gambling, alcohol, tobacco, or arms manufacture. To meet with Islamic law requirements, finance needs to be structured as a lease where rent and service fees are paid instead of interest or some other kind of profit-sharing arrangement. On Friday NAB will officially launch sharia-compliant loans of over $5 million for commercial property and construction, the first of the Big Four banks to do so. Fees and charges may apply, as well as terms and conditions which you should review. In order to open a credit product in future, you will need to meet our credit criteria and be approved. Please review the product disclosure documentation provided at the time of opening your account for detailed information. Chief executive Dean Gillespie says the bank already has a customer waiting list of 5000 and hopes to open next year. “There are developers that we work with that in the past just haven’t used any bank finance so we deliver projects with 100 per cent of their own equity,” said managing director Amen Zoabi. When Professor Ishaq Bhatti came to Australia 30 years ago, the bank teller looked bemused when he asked for a savings account that didn’t accrue interest. When Professor Ishaq

0 Comments

Leave a Reply. |

ArchivesCategories |

RSS Feed

RSS Feed